i2Live

More choice and control in retirement

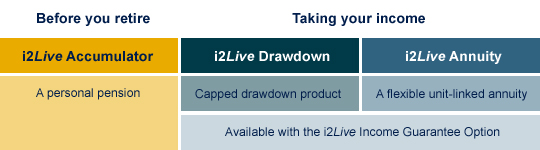

i2Live is designed to give you more choice and flexibility as you move through your retirement. It consists of three retirement planning products:

- i2Live Accumulator - a personal pension.

- i2Live Drawdown - an income drawdown product.

- i2Live Annuity - an investment-linked flexible annuity.

Before retirement

i2Live Accumulator consolidates all of your pension savings into one single plan, making it easy to convert all or part of your retirement fund to i2Live Drawdown or i2Live Annuity when you want to start managing your retirement income.

Taking your retirement income

Although i2Live is no longer open to new customers, existing i2Live customers can move from one to product to another. Please note that you will now only be able to convert from the i2Live Accumulator to the i2Live Drawdown if you already have an existing i2Live Drawdown (one that has previously received a conversion from the i2Live Accumulator).

On retirement, you can choose to take a flexible retirement income without being locked into one annuity rate and keep your funds invested in equities through i2Live Annuity or i2Live Drawdown.

Both of these products have an Income Guarantee Option.

Income Guarantee Option

Enjoy the security of a guaranteed income

For many of us, retirement is full of possibilities – travel, new hobbies, perhaps spending more time with our grandchildren.

It is also a time when we need peace of mind, knowing that we’ll have enough money to live comfortably.

When you choose i2Live Drawdown or i2Live Annuity, you can opt to add an Income Guarantee Option for an annual charge. This gives you the reassurance of a minimum level of income, whether investments fall or rise in value.

Better still, your pension remains invested and still has the potential to grow. So, unlike a conventional level annuity that pays a fixed income for the rest of your life, your guaranteed minimum income could rise if your funds perform well during each five year review period.

Features of the Income Guarantee Option

- A guaranteed minimum level of income (GMI) - no matter how your investments perform.

- Apply the guarantee to all or part of your i2Live Annuity or i2Live Drawdown funds.

- Switch the guarantee on and off when you want to and only pay for it when it's switched on

- There is an annual charge of 0.95% on the funds to which the guarantee applies.

- The Guaranteed Minimum Income level is reviewed every five years and may increase if your funds perform well.

- When the guarantee is selected, a maximum of 60% of funds can be invested in equities (or funds of a similar risk to equities).

i2Live retirement solutions invest in unit-linked funds, which means the value of your pension fund can go down as well as up and is not guaranteed. i2Live retirement products are only available to existing i2Live customers.

Fund hub

Disclaimer

You are being redirected to a website external to Sun Life Financial of Canada.

The content of this fund hub is for information only. It is not designed to provide advice on the suitability of an investment for your personal financial situation. Please contact your financial adviser for further explanation or advice if you want to know if a fund is, or remains, appropriate for you.

Unit prices can fall as well as rise on a daily basis and are not guaranteed. Charges and costs may also vary.

Whilst every care is taken in the calculation and publication of these figures, Sun Life Assurance Company of Canada (U.K.) Limited and its sources accept no liability arising out of any error, inaccuracy or mis-statement contained in it or any usage of the information.

By clicking continue below you agree to our online usage terms and conditions.

Our fund hub provides fund fact sheets for all our unit-linked and i2Live funds. Use the fund hub to find the latest unit prices, past performance data, fund charges and information about our fund managers.

Finding your fund code

You will need your full fund code to find your fund fact sheet in the fund hub. You can find the main part of your fund code in your annual statement. The full fund code will depend on where you bought your Sun Life Financial of Canada plan from originally or the type of product you have.

Who did you buy your original plan from?

For customers who bought plans directly from Sun Life Financial of Canada or Confederation Life:

- If the fund code in your annual statement starts with a letter you don’t need to add anything to the beginning of the code. You already have the full fund code and can use this to find your fund fact sheet.

- If the fund code in your annual statement starts with a number, please:

- Add the letter A to the beginning of your code.

- Make the number three digits, for example ‘1’ is 001.

- If you have accumulation units add A at the end of your code or if you have capital units add C at the end of your code. If you are not sure which type of units you have, please give us a call.

For example, if the fund code on your annual statement is ‘38’ and you have accumulation units, your full fund code is A038A or if you have capital units your full fund code is A038C.

For customers who originally bought plans from one of the companies we now own shown in the list below:

| Armco | Laurentian |

| Associated Investors | Liberty |

| British National Life Assurance (BNLA) | Life & Equity |

| Cannon | Lincoln |

| Citibank | Southampton |

| City Financial | Trident |

| Imperial | Trinity |

| International Life | Yeoman |

- If the fund code in your annual statement starts with a letter you don’t need to add anything to the beginning of the code. You already have the full fund code and can use this to find your fund fact sheet.

- If the fund code in your annual statement starts with a number, please:

- Add the letter B to the beginning of your code.

- If you have accumulation units add A at the end of your code or if you have capital units add C at the end of your code. If you are not sure which type of units you have, please give us a call.

For example, if the fund code on your annual statement is ‘001’, your full fund code is B001A.

I am an i2Live customer

You can find the main part of your fund code in your annual statement. Your fund codes start with an F followed by 3 numbers (e.g F848). You need to add an A to the end of this code (e.g. F848A).

Not sure?

If you are not sure or have any questions, please give us a call. We can look your plan up and tell you your fund code.

Capital or accumulation units

The value of your plan could be invested in either capital or accumulation units, or a mixture of the two. This will depend on your individual plan and the type of contributions made.

Capital units have a higher Annual Management Charge to cover our costs for setting up your investment. We have shown the difference in these charges within the fact sheets. The performance figures demonstrate the performance of the fund, after allowing for the impact of fund charges.

If you are not sure which type of units you have, please give us a call.

This guide aims to make the cost of investing in our funds transparent. It provides more detail about the charges involved when you invest in a fund and what this means for you. We want to help you make informed choices and hope that you find this guide useful.